Mintos review – Results after investing €6,000 over 44 months (2021 Update)

Last update: August 19th, 2021.

Table of Contents

❓What is Mintos?

Mintos is a worldwide peer-to-peer (P2P) marketplace with its headquarters in Riga, Latvia. It was launched in 2015 and has grown steadily since then. Today, Mintos has 38% of Europe’s P2P market share, which makes it one of the largest if not the largest P2P platform in Europe. With an average interest return rate of 11.61%, Mintos gives you some of the best opportunities to spread or diversify your investment portfolio. It has very functional features make it one of the best P2P lending platforms for both beginners and experienced investors.

According to the platform’s CEO and Co-founder Martin Suite, Mintos is currently focused on becoming the best P2P platform in the world. That’s why they continue to invest more on their products and technology rather than focus on making profits. But even with that, Mintos experienced an increase in its revenue to over €2.1 million just three years after its launch! To make it even better for investors, the platform tripled investments to over €4.8 million new loans in 2018 compared to €1.6 million in 2017. This is perhaps a clear indication that Mintos has a great model that’s working just perfectly in the challenging P2P lending marketplace.

Like most P2P lending platforms, Mintos does not originate loans directly to borrowers. Instead, it works as a middleman that connects borrowers looking for capital to grow their business with investors looking to invest their money to make profits. In other words, Mintos is a simple platform where external loan originators sell their loan shares. The platform is also one of the most diversified as it offers loans from 70 loan originators operating in over 30 countries including the UK, Mexico, Estonia, Latvia, Finland, Poland, Kenya and many more.

As an indication of how great Mintos is as a P2P lending platform, the platform won AltFi’s People’s Choice Award for three consecutive years in 2016, 2017, 2018 and for the forth time in 2020.

Also, Mintos won the AltFi 2019 Alternative Finance Platform of the Year award. The platform has also been named as the “Most Influential financial start-up at the Spanish Fintech Awards in 2018. This perhaps is a superb sign of how Mintos is doing great things in enhancing Europe’s P2P lending marketplace.

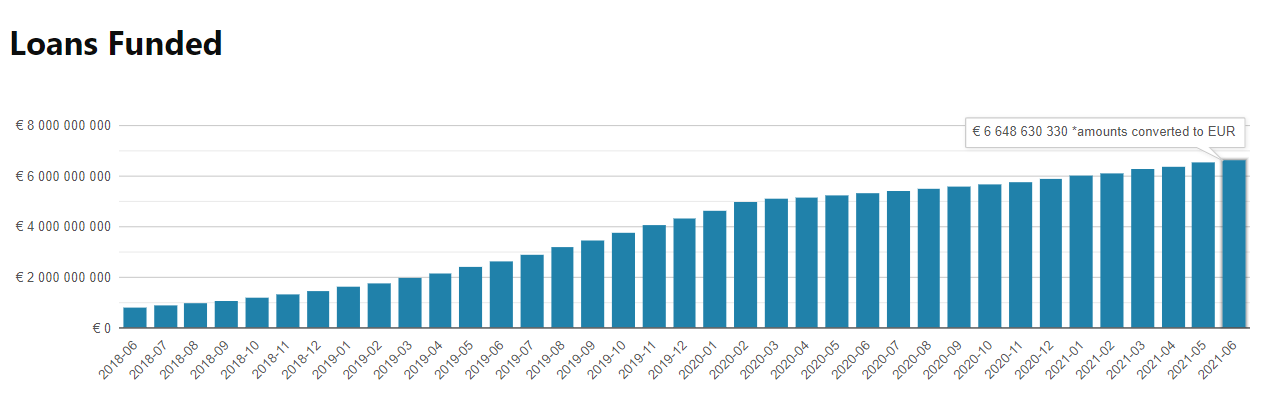

With over 413 000+ registered investors spread in over 62 countries, Mintos has, so far, facilitated more than €6.6 billion worth of investments.

It has also raised over €7 million to enhance its growth in the marketplace. For instance, the platform raised €5 million in November 2018 to create and provide its users with debit cards and personal IBAN accounts. As such, Mintos has a plan in place to enter the digital banking industry, which will allow users to make online transactions while also withdrawing money through their ATMs. The platform also has an e-money license in place, which makes it one of the most secure platforms out there.

Are you already thinking that Mintos could be the best platform for you? Well, read on and find out more.

🔑 Mintos key facts

As mentioned earlier, since launching in 2015, Mintos has demonstrated exponential growth and has become the world’s largest marketplace of its kind.

As an investor, it’s of great importance that you carry out some thorough research on any given P2P platform before even considering investing on the platform. By doing this, you’ll become aware of various issues and statistics such as any applicable fees, the number of loans funded and even investor statistics.

- Launched in 2015;

- Total invested € 6 457 491 241;

- Founders: Martins Sulte (CEO), Martins Valters (CFO);

- Over 190 employees;

- Headquarter: Skanstes 50, Riga, LV-1013, LV;

- Over 406 000+ investors from 62 countries;

- Incomparable diversification possibilities;

- “Excellent and great” – 90% on Trustpilot;

- Auto invest feature;

- Secondary market;

- Buyback guarantee available (but not for every loan);

- Minimum investment 10€.

How well did Mintos do in 2019?

2019 was a superb year for Mintos, just check out the infographic displayed below:

⚙️ How Mintos Works?

As I have noted, Mintos is a P2P lending platform that doesn’t originate loans. While it doesn’t connect borrowers directly to investors, it works a marketplace where lending companies (loan originators) of the already funded loans to investors. With many loan originators available on the platform, a borrower applies for a loan from one of the originators.

The loan originator will perform due diligence on the borrower to assess and evaluate the risks. If satisfied, the loan originator will issue the loan to the borrower from their fund and at a predetermined interest rate. These loans are then listed on Mintos where you can invest in a particular loan based on an assigned agreement, which will guarantee you monthly payments and interests.

Unlike most P2P lending marketplaces, Mintos focuses on the functionality of its platform to enhance user experience. That’s essentially why it has 14 filters that can help you choose the most suitable loan. Whether your focus is on the interest rate, Mintos’ ratings, country, buyback guarantee, loan terms, loan types, loan originators, borrower APR, amortization method, loan status, LTV ratio, listing date or investment structure, the platform gives you various ways to filter what works best for you.

To make it much easier for you, here’s a breakdown of how Mintos work

Third-Party Lenders

It’s important to emphasize that Mintos is not a lender. Instead, it acts as some sort of a middleman between you, the investor, and third-party lending companies. Simply put, third-party lending companies (also known as loan originators) issue loans to businesses and individuals but use Mintos to raise capital. As an investor, this allows you to invest in any type of loan that suits your interests.

Here’s a perfect example. Laxo, a loan company in Finland, has plans to issue a €15,000 business loan to a start-up company known as Vamon Enterprises. Laxo will perform due diligence on Vamon Enterprises without involving Mintos in this due diligence. If Laxo approves to issue the loan to Vamon Enterprises, the loan will be then listed on Mintos to help raise capital.

Investors

Once the loan has been listed on Mintos, you as an investor or registered member will make your investment, which is to principally raise capital for the borrower. This gives you an option to invest and diversify your investments in various types of loans including mortgages, car loans, and personal loans.

Making an Investment

As an investor, all you need to do is find a loan type or structure that suits you. With as little as €10, you can invest in various types of loans. It doesn’t matter how much you have, your investment will be pooled together with other investors on the platform to finance the loans that you choose.

⚙️How to Invest through Mintos

To enhance user experience and the general functionality of the platform, Mintos offers you and other investors investing styles such as Auto Invest, Mintos Invest & Access, and Manual Investing.

Let’s briefly go through them.

Auto Invest – This can be a great way of investing in Mintos if you do not have time to go through the loans regularly. In other words, you will use a pre-defined strategy to invest in loans that perfectly suit your portfolio. The platform allows you to choose the types of loans that might be of interest to you, the amount of money that you want to invest, and more importantly, the loan terms.

By choosing this way of investing, you’ll not have to manually go through the process of investing whenever an appropriate loan appears. Instead, the platform will automatically do it for you but only based on the predefined strategies that you chose. Generally, the most common types of auto-invest strategies that are used in Mintos include Diversified Strategy, Short Term Strategy, and Secured Loan Strategy.

Invest & Access – On 10th of June 2019, Mintos came out with a new product called Mintos Invest&Acccess. This can be a superb way of investing if you’re likely to require your money before the investment period matures. It is fully automated and doesn’t lock your money in a particular loan for a very long time or until maturity. All you have to do is select the amount that you’re willing to invest and the list of loans that match your criteria will be provided. The best part of using this type of investing is that your investment can be sold to other investors before the maturity date if that’s what you want. However, the minimum portfolio size has to be €500.

Mintos Invest&Access is a similar product to Bondora’s Go & Grow, except Mintos Invest and Access offers returns up to 12% instead of Bondora’s 6,75%.

Read more about Mintos Invest and Access here – https://financefreedom.eu/mintos-invest-and-access/

Manual Investing – Unlike the two ways of investing explained above, which are done automatically based on predefined criteria, manual investing gives you the chance to personally choose and pick the type of loans that are suitable for you. You have to do it manually, which means you’ll have to spend more time on the platform looking for what might be of interest to you.

A Great Platform for Diversification

In addition to having a wide range of loan originators, Mintos gives you an excellent opportunity to diversify in various types of loans. This is, of course, essential, in spreading your risks and choosing the types of loans that suit your preferences.

Some of the loans offered on the platform include:

-

- Business loans – Highest rated LO’s: 1pm plc, Mikro Kapital.

- Personal loans – Mogo, Banknote, BB Finance Group, Credissimo, Everest Finanse, Placet Group.

- Mortgage loans – ACEMA, Extra Finance.

- Agricultural loans – AgroCredit, Mikro Kapital.

- Short-Term loans – Banknote, Credissimo, VIZIA.

- Pawnbroking loans – Banknote.

- Invoice Financing – EBV Finance, Capitalia.

- Car loans – Mogo, IuteCredit.

What happens when a Loan Originator goes belly up?

It is unlikely that a Loan Originator will go bankrupt, but it has happened! P2P lending is growing fast and whichever company can’t keep up with the pace, will most likely suffer the consequences.

Since Mintos launch from the beginning of 2015, more than 5 years after, Mintos has experienced problems with few loan originator: EUROCENT and Metrokredit.

You can find more information about the two Loan Originators in the Mintos Blog and about Metrokredit.

What Rate of Returns to Expect

Given that most investors on Mintos receive a net annual return of around 11.91%, this is the same rate that you can also expect. Note that this is just the average rate. You can, however, expect a higher rate of return if you’re willing to risk more of your money in loans with higher return rates.

That being said, there are over thousands of different types of loans on Mintos that offer over 18% interest rates. So depending on your risk appetite, you can choose such loans.

❓How to create an account on Mintos?

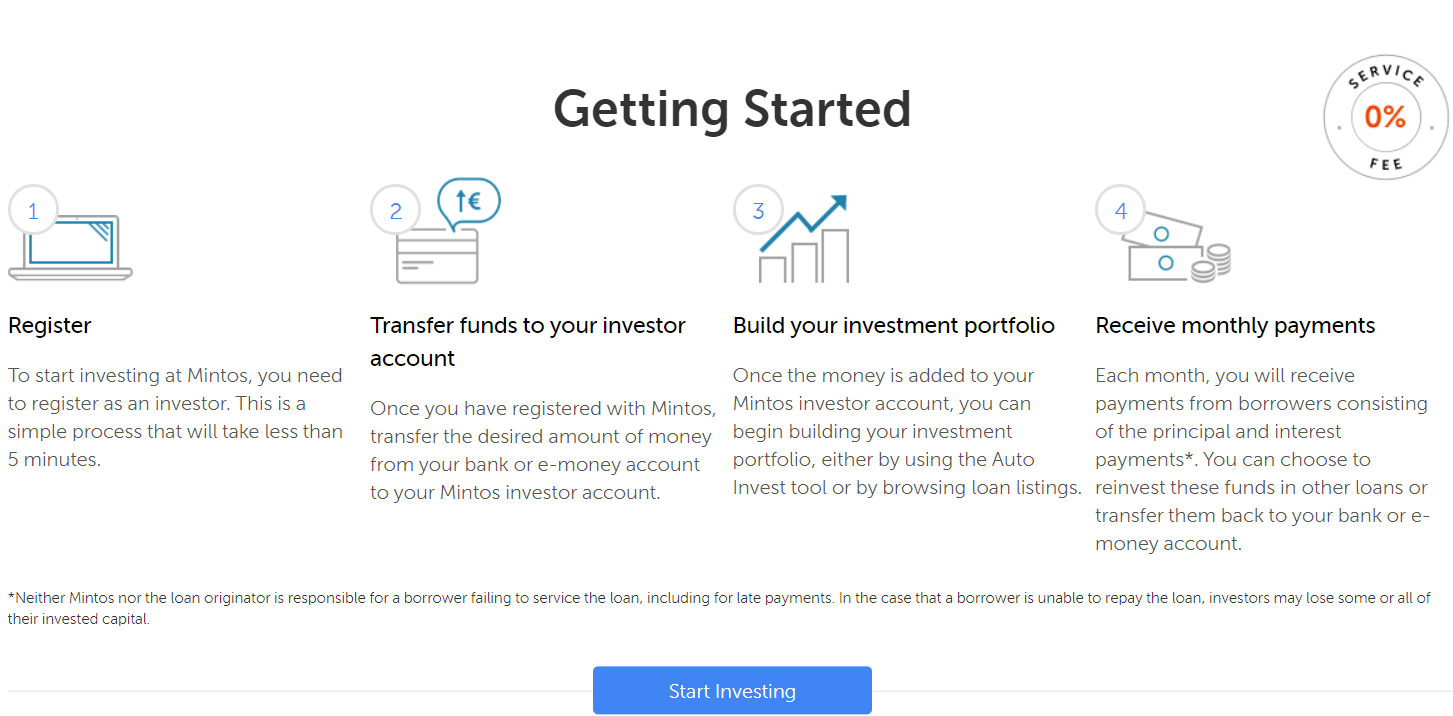

You’ve probably gained some interest in using Mintos as your P2P investment vehicle, but that’s not enough. You’ll have to create either an individual or company account on the platform. The process is so simple. All you need is a working email address, choose the account type (individual or company), enter your name, create a password, fill in your country of residence, agree to the terms and conditions, and click register.

It is very easy. All you need to do is fill out Mintos registration form here.

There are total of 4 easy steps:

1. Use your email address to create an account;

2. Verify your ID by providing Mintos with a copy of your driving license or passport and a proof of current address, for example utility bill or bank statement;

3. Make a deposit to your Mintos account. It can be done with a SEPA transfer or using money transfer services, for example Revolut or Transferwise;

4. Choose an investing strategy and start investing on Mintos!

Verification

Before you can use the account to invest, you must verify your account. You’ll have to fill in information about your employment, source of fund, and of course, you’re a scanned ID or passport. Your verification will be done through your smartphone camera or webcam. So it’s essential to make sure the details in your ID and passport are visible and the room is well lit. In most cases, it may take up to 10 minutes to complete the entire process.

How to transfer money to your Mintos account?

You can transfer money to your Mintos account from your bank or e-money account. Transfers in EUR can be done easily and at low cost using SEPA (Single Euro Payments Area) transfers. If you have money in currency other than EUR, you can transfer it using money transfer service, for example Revolut or Transferwise.

Who Can Invest in Mintos?

As we’ve noted, you can invest through Mintos as an individual or as a company. You’ll, however, have to be at least 18 years, have an identification document (ID or a passport) and have an active bank account in the SEPA region (you can check them out). For companies, they must be registered in the EU or countries operating under AML/CTF regulations. Keep in mind that the platform (like most P2P lending platforms) is accepted neither in the UK nor U.S.

Loan Liquidity

Loan liquidity is one of the most important factors to consider when choosing an appropriate P2P platform. With that in mind, Mintos is perhaps the most liquid P2P platform today. This platform has over 400,000 loans in the primary market and over 300,000 loans in the secondary market. This means that you can easily find a loan to invest in in the primary market so your money won’t stay idle just because there are no loans to invest in.

Similarly, the secondary market gives you the chance to easily sell your portfolio either at a discount or a premium.

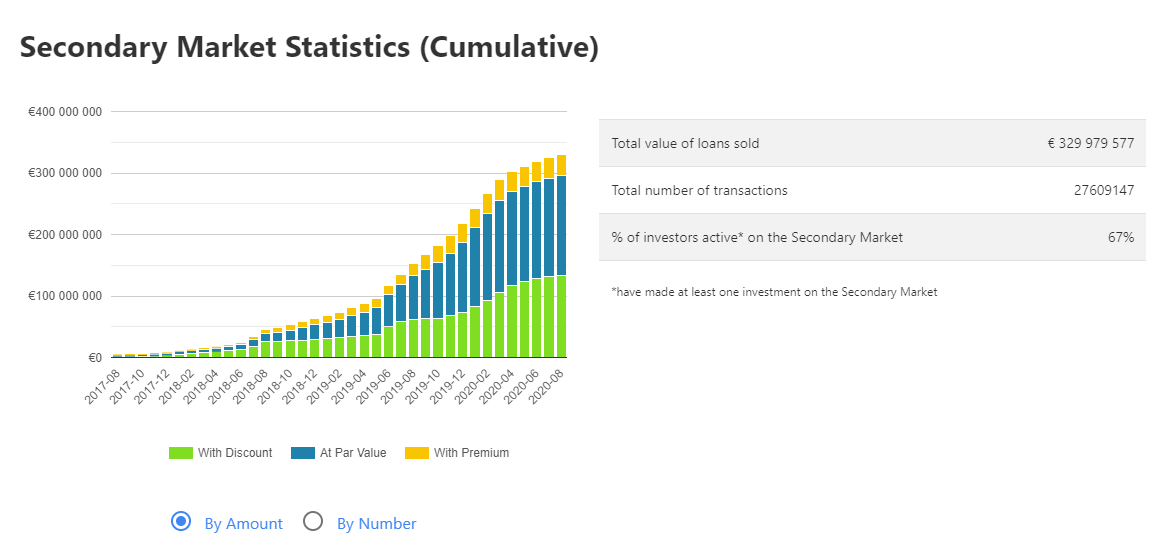

Mintos Secondary Market

Like most P2P lending platforms, Mintos offers a secondary market. This is of great importance for investors who are looking to sell or opt-out of their investments before the maturity date. The best part of the Mintos’ secondary market is that it’s bigger than the platform’s primary market. This means that it’s a perfect avenue to sell your investment at a profit. Again, it gives you the chance to easily liquidate your investment fast if say, you need some money for an emergency.

Benefits to investors selling loans on the secondary market include:

– more liquidity for their investments, whichever allows access to funds when necessary;

– opportunities to profit by selling investments at a premium.

Benefits to investors buying loans on the secondary market:

– opportunities to make investments in loans not available on the primary market;

– opportunities to profit by buying loans at a discount.

Mintos Auto Invest

Another important feature of Mintos is that it offers Auto Invest. This is to enable you to take a hand-off investment approach where all your investments will be done automatically based on predetermined factors. For instance, you still have the final say on how much is to be invested, the type of loan, the loan originator and so on.

The Auto Invest feature can be superb for you if you do not have enough time on your hand to invest manually. Again, perusing through the large volumes of loans that are available on the platform can be tiresome. With the Auto Invest, you can set up several portfolios not just in the primary market but also in the secondary market.

Here are the best strategies to apply when using the Mintos Auto Invest feature.

Secured Loan Strategy – This is for loans that are secured with collateral and have a Loan-to-Value (LTV) ratio of not more than 75%. The loan should have an interest rate of 7% or more with an average maturity rate of 40 months.

The Diversification Strategy – This is a perfect strategy if you’re looking to achieve a very high level of balance and diversification of your investment portfolio in terms of risk and return. Most of these loans guarantee an average annual interest rate of 8.5% with a maturity term of 25 months.

The Short Term Strategy – This can be a perfect strategy for you if you’re looking to invest only for a few months. Unlike other strategies, the average loan terms are very short (3 months or less) and with an average interest rate of about 7%.

How to Set Up Auto Invest Feature

It’s fairly easy.

Choose the currency, select the market, your preferred loan type, buyback guarantee (if you want a more secured loan), rating, and your preferred loan originator.

Do not forget about the interest rate setting, which is at the bottom of the page. This is essential if you want to select your preferred interest rate. You can also select other features such as the minimum or maximum amount that can be invested, your preferred strategy, portfolio size, and whether or not for the profits to be reinvested.

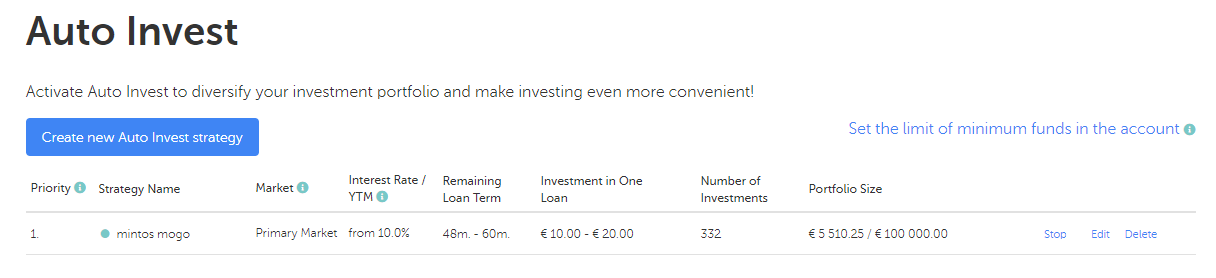

My strategy on Mintos P2P platform is to spread the risk between different Loan Originators. My Mintos Auto Invest settings. Take notice that this is not any specific advise to where and what to invest in.

My preferred Mintos Auto Invest settings

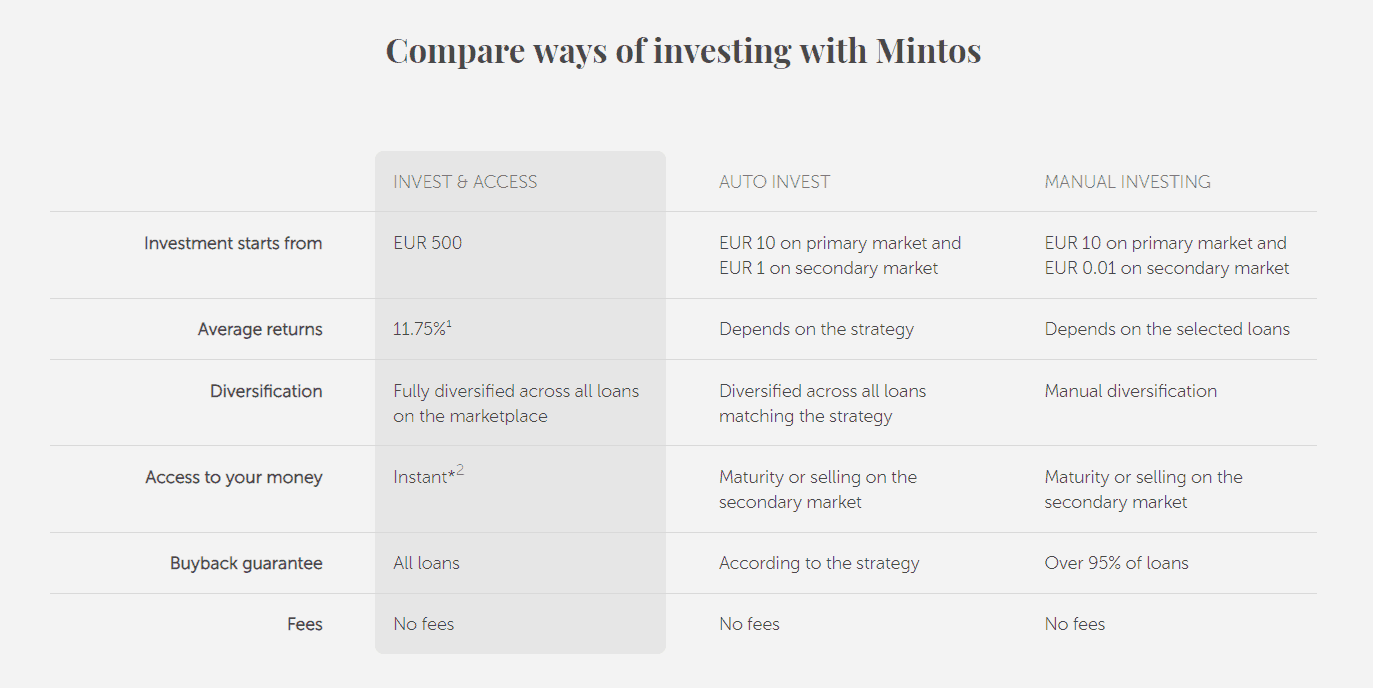

Mintos Invest&Access vs Auto Invest vs Manual Investing

(click on the picture to magnify)

Mintos Buyback Guarantee

Mintos guarantee investors that they’ll get their money back if the borrower defaults. Generally, the loan originator should buy back the loan if the borrower fails to pay within 60 days. You should, however, keep in mind that some loan originators will not pay interest if there’s a default. In other words, you’ll get your money back with interest.

And although most loans have buyback guarantees, some of them do not. For instance, you’ll find that less than 100 loans out of more than 300,000 are not covered.

How is interest calculated?

Interest is calculated on a daily basis. It is measured against the amount you have invested in loans on the respective day.

In contrast, the formula for calculating interest is as follows: Invested amount * Amount of days * Interest rate/360.

🔒So what are the Risk Mitigation Plans?

Given their high level of transparency, Mintos makes it quite clear that on the website that there are certain risks associated with investing through the platform. As such, the platform has a wide range of risk mitigation layers in place to make the platform as secure as possible.

Buyback Guarantee – The first and most important step is the buyback guarantee that ensures that investors get their payment even if the borrower defaults.

Skin in the Game – Mintos also has measures in place to ensure that their skin in the game works perfectly. They do this by ensuring that all the loan originators keep a given percentage of each loan (usually 5%) on their balance sheets.

Due Diligence – Mintos make it a priority to ensure that they perform thorough due diligence on loan originators to ensure that only quality and trustworthy loan originators are accepted onboard. And even with that Mintos continuously monitor both the financial and general performance of the loan originators to ensure that the required quality and professionalism are upheld.

💡What does the Mintos Rating measure?

Mintos is probably the only P2P lending platform that rates its loans to help investors assess the risk level. Running from A+ (lowest risk) to D (highest risk), this rating system is to help you asses the performance of the loan originators and not the end borrowers. The main importance of this rating system is to help you determine the ability of the loan originator to pay even if the borrower defaults.

![]()

Low risk

A financially strong company, having a stable and leading market position, solid asset quality, robust debt collection procedures lead by a management team with a good track record and operating in stable and established regulatory environment.

Moderate risk

A company with stable but somewhat weaker financials and/or an average market position, and/or adequate debt collection procedures, and/or shorter asset quality track record lead by a management team with relevant experience and/or operating in a less regulated and/or uncertain environment.

Elevatedrisk

A company with considerable weakness in financial performance and standing, with limited competitive position and/or asset quality below the average and/or a limited track record, management lacking experience, and/or operating under substantial regulatory risk due to uncertainty.

Default

A company in financial distress, having problems to fulfill financial obligations and/or has defaulted.

Mintos assessment methodology is based of 5 different business factors with an individual weight:

- Operating environment (10%)

- Company profile (15%)

- Strategy and company management (15%)

- Risk profile (20%)

- Financial profile (40%)

These 5 factors illustrates how Mintos operate with their loan originators. It is very clear that Mintos is focusing heavy on making money. They have 40% of their emphasize on the loan originators financial profile, followed by the loan originators risk appetite. 2 factors that can impact the economics of the investors easily.

Ultimately, the Mintos Rating measures the counterparty risk or risk of loss resulting from a loan’s originators’ failure to service and/or transfer the received payments from borrowers to investors or meet other contractual obligations (including but not limited to the buyback obligation). Counterparty risk is capturing operational and default risk of the company acting as a loan originator, servicer of loans and obligor of the buyback guarantee to investors. The materialisation of those risks would cause a disruption in loan servicing and the buyback fulfilment which are the core risks related to loan originators on Mintos.

❌ What are the risks associated with Investing through Mintos?

As a wise investor, it’s always important to understand that high returns such as those available on Mintos do come with certain risks. It’s essential to take into account these risks and perform your due diligence before investing your money on the platform.

Here are some of the risks that you’re likely to encounter.

Borrower Defaults – Some borrowers may indeed choose to default and fail to pay back. Under such circumstances, you won’t have a lot of options but only to hope that the loan originator has recollection procedures in place. This is essentially why it’s advisable to target loans with buyback guarantee. This means that you’ll, at least, get your money back even if a borrower defaults.

Loan originator bankruptcy – A loan originator can go bankrupt, which can affect the investors. However, Mintos have measures in place to ensure that investors continue to receive their payments even if the originator goes bankrupt.

Interest Rate Risk – Some of the loan terms on Mintos can be as long as 5 years. In such scenarios, there’s a possibility that the preset interest rates could fluctuate as a result of inflations in various economies. This is something that Mintos or the loan originators have no control over.

Liquidity Risk – Mintos’ secondary market allows investors to sell either at a discount or premium. Unfortunately, you’re more likely to lose a given amount if you decide to liquidate your entire portfolio.

Poor Diversification – Diversifying your loans is one of the best ways to spread and minimize your risks. But if you’re enticed by the high-interest rates and invest a substantial amount on a single loan, chances are you might feel the pinch of not diversifying.

Mintos Bankruptcy – Although it’s less likely that Mintos will go bankrupt, this is an idea that investors must have in mind. Fortunately for investors, Mintos has a backup plan in place to ensure that all investors receive their full payments in the unlikely event that the platform goes bankrupt.

Recession in the Financial Industry – If there are financial downturns like the one witnessed in 2009, chances are many borrowers may default, loan originator might go bankrupt and this could spell doom for investors’ returns.

What was new at Mintos in 2020?

Mintos is, without a doubt, one of the most innovative P2P platforms. It always strives to make its marketplace much better. After introducing the Invest & Access feature in 2019, the platform now has plans to introduce debit cards in 2020. This will make it quite easy for investors to access their profits.

The platform is also currently working on a mobile app. This is central to Mintos 2020 projects and will become a significant differentiator in the industry. This will make Mintos even much better as you’ll have the most important statistics about your investments on your fingertips. You’ll be able to operate your account on the app and even be able to deposit or withdraw directly from the app. Given that most people operate almost everything through their smartphones; this is a forward step that will enable Mintos to reach an even wider audience.

Things that Need Improvement

Despite being one of the best platforms, there’s still room for improvement.

More Info on Loan Originators and their Loans – It would be better to provide more information on loan originators such as audited statements. There should also be more info on loan default rates and recovery rates, as well as the country of origin.

Better Statistics – While there are lots of statistics provided by Mintos, it would be better to provide even more statistics on issues such as the exact number of investors, investment volumes, the number of loans issued monthly and many more.

Ownership Transparency – The ownership of Mintos is a thorny issue that has never been clearly stated. Mintos should improve on this by stating who the real owners of the platform are.

Better Regulations – Although Mintos adhere to financial regulations of Latvia where it’s registered, the platform should strive to adhere to some of the world-recognized financial regulations such as the FCA in the UK. This will be better in the sense that the platform will be allowed to accept investors from the UK and the US, which it currently doesn’t have.

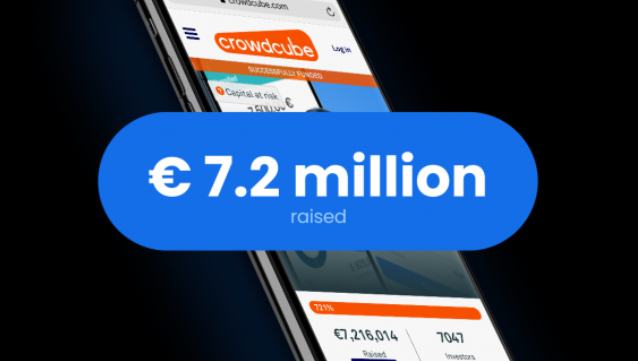

Mintos crowdfunding campaign at Crowdcube

In November 2020, Mintos announced that they will be crowdfunding on Crowdcube to accelerate growth and to develop new products.

In a crowdfunding campaign that exceeded all expectations, Mintos set a new record on Crowdcube. During the 10-day stretch, the crowdfunding campaign attracted over 7000 equity investors and raised a total of €7.2 million, the largest amount ever raised in continental Europe.

More information about the Mintos crowdfunding campain – https://www.crowdcube.com/companies/mintos/pitches/qDJxrZ

Mintos Pros

- Huge loan volume;

- Predefined investing strategies;

- Huge number of originators;

- Auto Invest feature to make it easier for you;

- The secondary market is very active;

- There are no fees;

- The buyback guarantee makes the platform secure;

- It has a profitable business model.

Mintos Cons

- The interest rates can fluctuate;

- The platform charges currency exchange fees;

- Tax reporting is not uniform;

- Using Auto Invest can be quite challenging for newbies.

Mintos Competitors

If you’re skeptical about using a single P2P platform and would love to diversify across the platforms, you can consider choosing Bondora, Twino, and Peerberry.

Mintos review: Conclusion

Having followed Mintos from when it was launched and seen it grow from strength to strength, I can say without bias that it is one of the most innovative P2P platforms if not the best. The large volumes of loans that are available on the platform certainly make it possible to reduce the risks by diversifying your portfolios. The interest rate that’s offered by Mintos is also one of the best in the industry and should be attractive enough if you’re looking for an investment that guarantees better returns.

The platform’s features are also among the best in the industry. From buyback guarantee, Auto Invest to predefined investment strategies, Mintos is a great platform that will work perfectly for you. We highly recommend it and hopefully, it will help you attain your financial freedom.

In my opinion, Mintos is one of the absolute best P2P platforms available right now.

So far Mintos has not disappointed me, they are transparent, direct and have a great net annual return rates. My average rate on the platform is 9.98% (As of 10th May 2021), which is pretty good and all my loans have buyback guarantee. In my opinion, Mintos marketplace suits well for beginners and the experienced investors.

If you are looking for even more comprehensive Mintos report, I suggest you to read Colminey’s TORCH Report: Mintos. Colminey takes an extremely deep dive into the Mintos platform and answers questions like: “How transparent is Mintos, how likely is it to collapse, and are they doing everything possible to protect investors?”

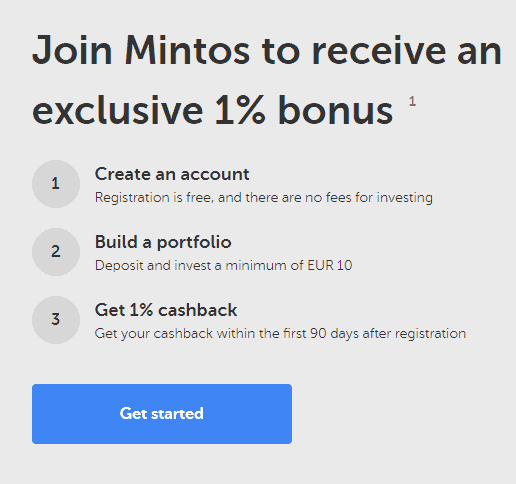

Join Mintos today and get 1% cashback bonus

Register here – https://financefreedom.eu/mintos/

![]()

Mintos gives you an exclusive 1% bonus on all investments you make within the first 90 days from your registration if you sign up through one of my referral links. This bonus can be found only here, you will not get this bonus if you sign up directly on Mintos.com

Click here to receive an exclusive 1% bonus!

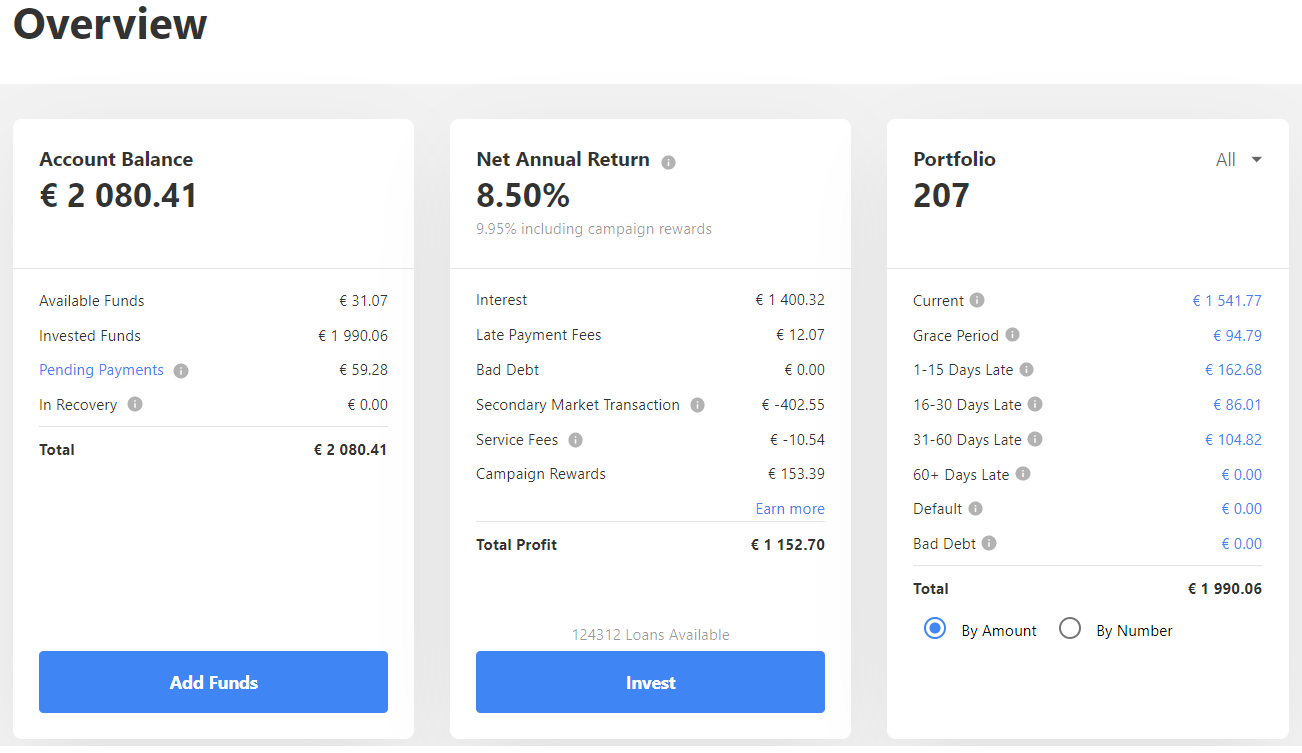

My account overview at Mintos.com:

You can see my portfolio here – https://financefreedom.eu/mintos-portfolio/

Your own thoughts

Do you have an account at Mintos? How big is your portfolio? Do you have any favorite Loan Originators? Let me know in the comments below.

Other options

My Portfolio for other investment opportunities. I also publish monthly updates of my portfolio.

invested 500€ into Invest and Access. Hoping for a decent ROI. Thanks for the review!

Been investing in Mintos for over 2 years for now and I must say that I have not had a single problem with them so far. Fingers crossed that the trend continues.

I am a holder of British passport, living in the Czech Republic. It seems that Mintos in unavailable for me – I even cannot create my account: both countries are not presented in their list…

Hey Olga!

I suggest contacting Mintos Help & Support – support@mintos.com

Well … I totally excluded Mintos from my investment platforms. 2 years ago it was an excellent platform, with an excellent rate of return. Since the covid appeared, everything has changed … to have money stuck in mintos … no thanks. Fortunately, there are many other p2p. My favorite is Bondora. The ease of withdrawing all my money at any time, and the simplicity of the platform are the big advantage.

They had delays during 2020 covid, luckily I had little invested during that time, but now everything is back to normal, no delays (at least not with my lending originators)…

At one time, I had 15K euro on Mintos, never had a problem, had to withdraw to buy a motorcycle hehe, withdrawal was very quick, deposit as well. Been investing since 2016. I do due diligence on the lending company I do business with on Mintos, to make sure they don’t go belly up. My auto invest is setup on loans that mature in three months, so I can get full withdraw within that period if I stop the auto invest. I only select loans with a buyback guarantee, and my average income percentage is a bit over 9%

Mintos is my favorite savings and investment tactic. I hope they stay that way.

Have to mention political risk – quite lot lending companies are from Russia and Belarus. Consider creating custom strategy that will not invest in countries that soon can be behind new iron curtain.