Grupeer Review: A Peer-to-Peer Lending Platform that’s Booming Fast

UPDATED!

Grupeer is a scam?! Nothing is 100% certain, but please read this article before making any decisions – https://p2pempire.com/en/review/grupeer/

Grupeer News – Is Grupeer Another Scam?

“Grupeer is currently facing serious accusations about the legitimacy of their loan originators (Monetria, Lion Lender, Epic Cash).”

Latest developments around Grupeer:

- Grupeer’s loan originator Finsputnik stopped offering the buyback guarantee.

- Grupeer has recenty changes their banking providers without much explanation. (Envestio and Monethera showed similar behavior before shutting down.)

- According to testimonials and LinkedIn updates, Grupeer has laid off several staff members in the recent days.

- Issues with withdrawals and late payments are increasing.

- Investors exposed the Promenada Project as a fake.

- On the 31/03/2020 Grupeer suspended all payments to investors. Grupeer is blaming the declaration of an emergency state in the European Union.

_________________________________

The fast and steady growth of peer to peer (P2P) lending in recent times has been nothing short of marvelous. The industry might be relatively young but it’s been growing by two digits every year not only in Europe but throughout the world! Part of this growth has been aided by the fact that saving accounts and traditional banking investments pay low returns. On the other hand, P2P lending platforms offer good alternatives for investors not just to diversify their investment portfolios but also to earn more. One such platform is Grupeer.

Established in February 2017, Grupeer is certainly one of the fastest-growing P2P crowdlending platforms. As of 2019, the platform has more than 21,450 registered investors and has issued more than 68 million euros in loans with average earnings of 13,19%. This is a tremendously huge growth considering that the platform only had 2,600 registered investors in September 2018.

As you can see, Grupeer is still a relatively new platform, which is growing nicely and establishing itself as a credible player in the P2P market. For this reason, let’s learn more about Grupeer, what it offers, and how to use it as an investment vehicle.

What is Grupeer?

Based in Riga, Latvia, Grupeer is a crowdlending platform established in February 2017 by brother and sister Andrejs Kisiks and Alla Kisika. This platform connects loan originators with investors and offers two main categories to invest in business loans and real-estate development projects. Most of these loans have maturity periods varying between 3 and 24 months and they all come with a buyback guarantee.

Key Characteristics

- Estimated Return – Up to 14% (Average 13.19%);

- Issued loans: 68 576 378€+;

- 21450 investors from 91 different countries;

- Accepted Currency – Euro (€);

- Early Exit – No secondary market;

- Minimum Investment – €10;

- Manual Invest – Yes;

- Auto Invest – Yes;

- Buyback Guarantee – Yes;

- Fees – No fees.

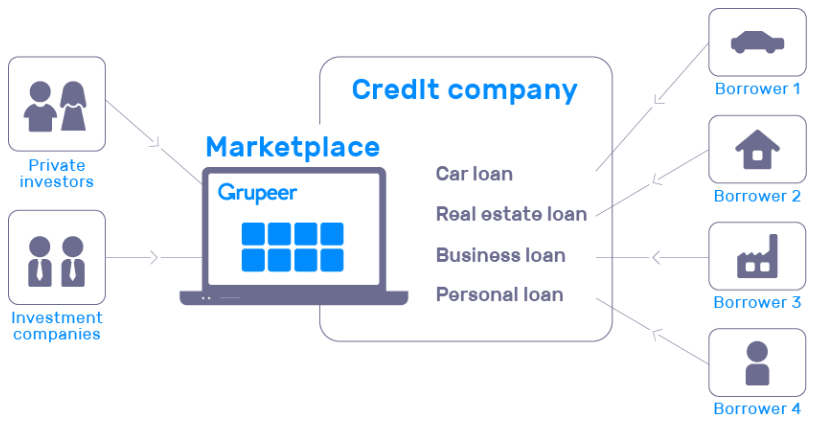

How Does Grupeer Works?

Grupeer is simply a crowdlending platform that connects businesses looking for funds with investors looking to invest. It is essentially an efficient online platform that offers investors numerous investment opportunities and the chance to make their own investment decisions.

The platform offers a simple and very easy-to-use interface, which makes it quite straightforward to find projects to invest in. To invest, you simply click on the invest-button, type the amount you want to invest, and click the “suitcase” icon to add the project to your basket. You can add as many projects as you can. You can confirm your investment once you’re satisfied with your choices.

Here’s a summary of how Grupeer works.

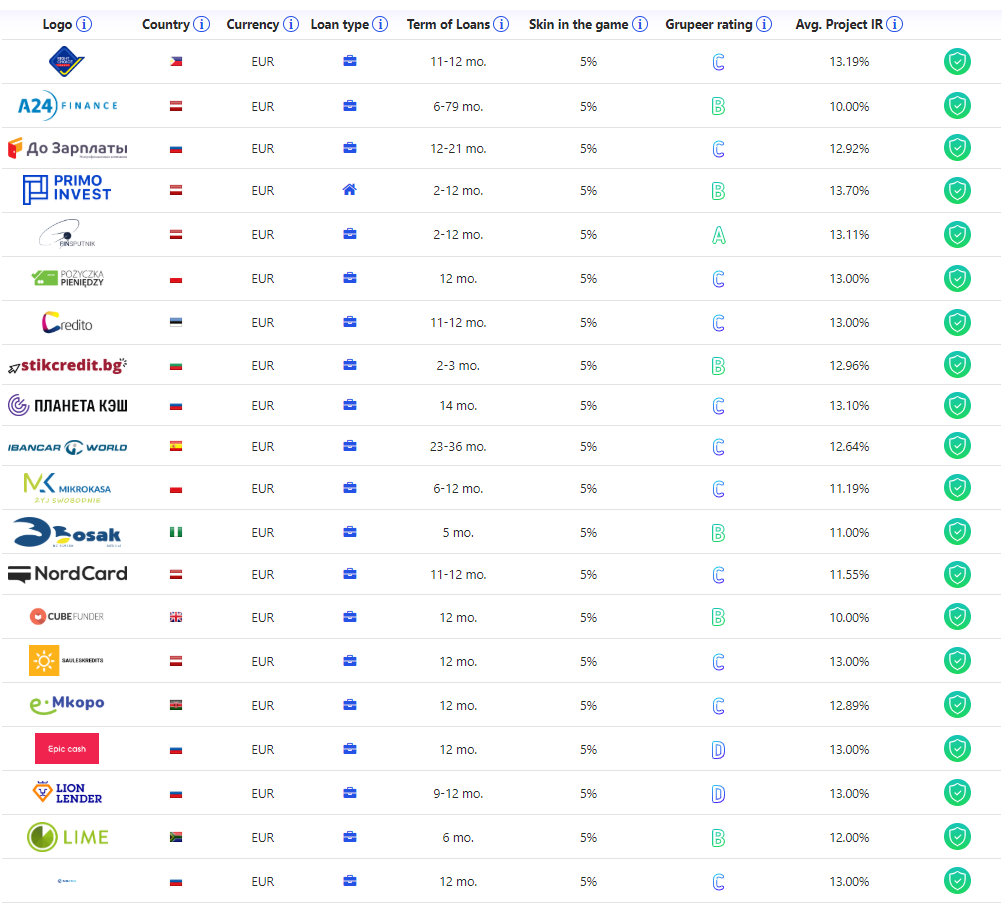

- Credit companies (generally known as loan originators) receive applications from businesses or individuals looking for car loans, mortgages or loans for businesses or personal expenses. Below are some of the loan originators;

- The Grupeer marketplace displays approved loans to investors on the platform;

- Investors can then view the displayed projects and choose the ones to invest in;

- Once an investor has invested in a particular project, a cession agreement that includes the loan collateral (This is an asset that the borrower offers as a guarantee for the loan. If the borrower defaults, the lender can seize the collateral and resell it to recoup the losses) is issued to the investor.

Below is an image of Grupeer’s business model.

Who Can Invest in Grupeer?

If you’re planning to invest in Grupeer and wondering whether you’re eligible, this is for you! Grupeer only accepts money transfers from countries within the European Economic Area (EU member states plus Switzerland, Norway, Iceland, and Liechtenstein). In fact, this is per AML (Anti Money Laundering) requirements. That being said, citizens from these countries can register and use Grupeer to invest. You can as well invest in Grupeer if you live in the EU or have an EU bank account.

It’s also worth noting that you can only use Grupeer if you’re 18 years and above. The platform also reserves the right to decline any particular application. If such a situation occurs, the platform will inform you accordingly either by phone or email.

How to Sign Up

Like most P2P platforms, signing up on Grupeer is extremely simple and easy. All you need is your name, an email account and you’ll have an account active. With this, you’ll be able to access all the available projects and details such as interest rates and loan periods.

You’ll, however, not invest until you pass the KYC (Know Your Customer) test, which requires you to indicate the origin of your funds and upload some identification, but this is after confirming your email.

Here’s the Grupeer’s account opening process:

Step 1 – As we’ve noted, Grupeer’s account opening process is simple, very easy, and requires little personal data. You need to provide your name, email address, phone number, country, and password. Grupeer will send you a confirmation email if your account opening is successful.

Step 2 – You’ll have to verify your identity after completing the registration form. You’ll have to scan your identity card and tax documents to verify your account.

Step 3 – You can then fund your account to start investing.

How to Invest in Grupeer

Here are the steps on how to invest in Grupeer.

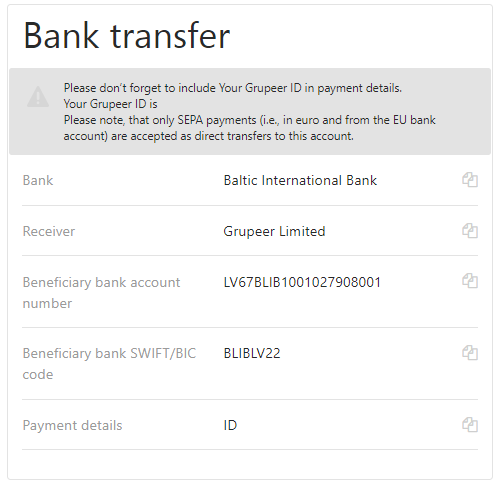

Deposit Money – You should transfer money from your bank account to your Grupeer account. It’s important to indicate your Grupeer account ID in your transfer comment. Given that Euro (€) is the primary currency on the platform; you should send your deposit from a Euro account. It generally takes 3-4 business days to receive the money on your Grupeer account.

And what are the possible ways of transferring money? Well, the only way to deposit or withdraw money from Grupeer is through a bank transfer (a confirmed bank account for withdrawals). In other words, you can only withdraw money to a bank account that you linked to your Grupeer account during the application process. It’s, therefore, important to include your genuine bank account when registering your account.

Choose the Project to Invest On – The platform offers a fabulous filter to help you easily choose your preferred investment type (business, mortgage or development loan). You can also click on the loan ID and view additional information on what you want to invest in.

Select the Investment Amount – Once you’ve selected the project(s) to invest in, you should decide how much you want to invest. It is, however, advisable that you diversify your portfolio to spread the risk.

Invest – Having confirmed your investments, you can view them on your dashboard. You’ll find information such as the amount invested, the ROI, the loan type, loan period, and the contract with the borrower.

Earn Interests – The platform pays monthly interest on your investment. Additionally, some investments also give you back a percentage of your invested money monthly but most of them pay the invested money at the end of the loan term.

Track Your Investment – The platform gives you the chance to easily follow your investment activities on your dashboard. This is of great importance in the sense that it offers useful information such as the available money and the money earned, as well as promotion programs.

What Products Does Grupeer Offer?

Given that Grupeer is one of the fastest growing P2P marketplaces in Europe, it offers diversified product portfolios which investors can choose from. Here are the types of investment options offered on the platform.

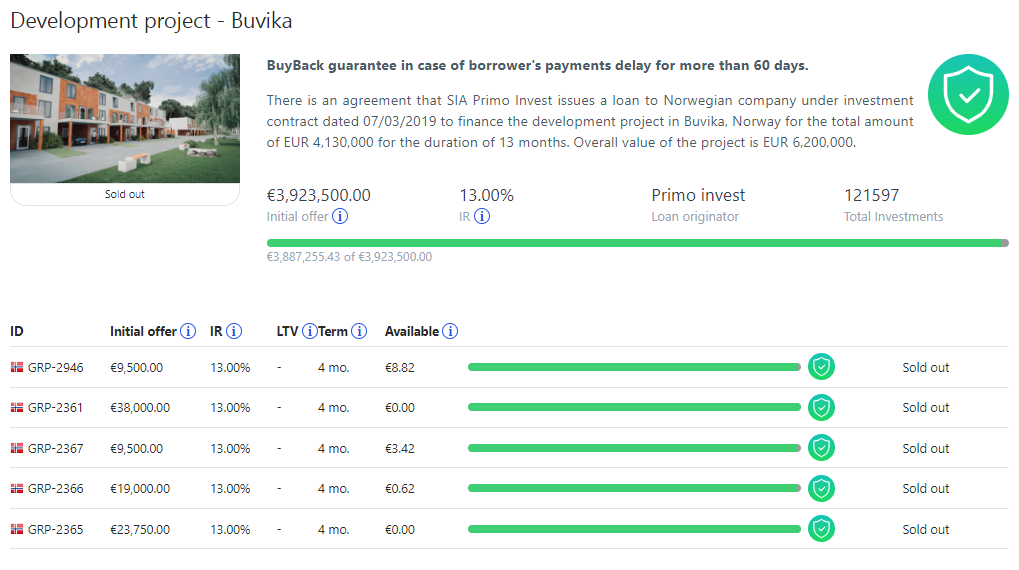

Development Projects

These are real estate development projects. They require higher amounts when compared to business and mortgage loans. Keep in mind that the rate of return and loan periods of these development projects vary depending on each project.

Loans

- Business Loans – These are typically offered to small and medium-sized businesses that have the capability of returning higher interests plus the principal amount;

- Mortgage Loans – Mortgages are, of course, one of the easiest ways to lend money to borrowers. Generally, these loans are secured by collaterals and often offer interest rates ranging between 10% and 15%.

Rate of Return

This is an important part of this review, especially if you’re looking to use Grupeer as your investment vehicle. Although the interest rates on Grupeer start from 10% they can go as high as 14%. The platform also runs periodic cashback campaigns (more on this later) that can help in boosting your returns, so it’s important to take advantage of them when they’re available.

Having talked about the rate of return, let’s briefly explain three different types of repayments used by Grupeer.

- Bullet – You get your interest paid every month but the principal amount is paid at the end of the loan period;

- Amortized – You get paid a given part of the interest and principal every month;

- Balloon – The interest and the principal is paid in full at the end of the loan period.

Loan Liquidity

Grupeer’s loan liquidity has improved immensely over the last few months. This means that your money won’t stay idle in the account just because there are no projects to invest in. This is because there are nearly 240 different loans available to invest in. Most of these loans are relatively large and can be as high as €100,000.

Buyback Guarantee

If the borrower delays to pay a loan for a duration exceeding 60 days, the loan originator is legally obliged to buy back your shares in the loan in the amount of the outstanding principal plus any interest accrued for the period of the loan. In short, most of the projects and loans offered on Grupeer come with buyback guarantees to ensure that your investment is secure even if the borrower defaults.

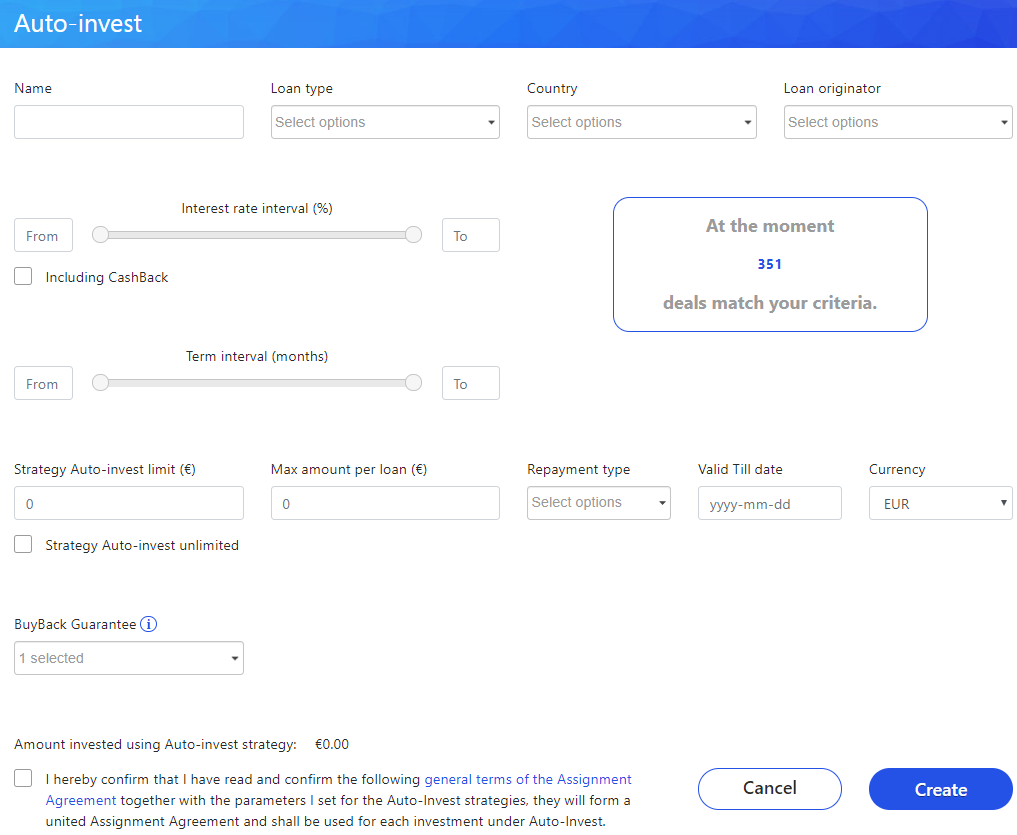

Auto-Invest

While we often encourage our readers to invest manually, Grupeer offers users the option to invest either manually or take advantage of its auto-invest feature. Nonetheless, you can choose to use the auto-invest feature and take advantage of its various investing strategies. For instance, you can choose to use auto-invest to invest in loans with higher interest rates or those with buyback guarantee.

Secondary Market

Unfortunately, Grupeer doesn’t have a secondary market and this is one of the platform’s noticeable drawbacks. This means that you cannot cancel or sell your loan once you’ve purchased the loan or before its maturity period.

Grupeer Cashback Campaigns

The platform has a bonus program known as Grupeer cashback, which the platform runs from time to time. If you invest in a loan or project that has a cashback campaign, you’ll receive the value back into your account. Typically, the cashback program has set conditions such as a specific timeframe that the offer is open, as well as the percentage offered (usually 1%).

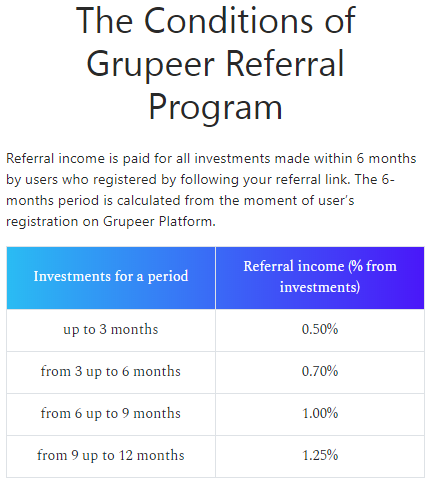

Grupeer Referral System

Like most crowdfunding platforms, Grupeer offers a referral program to its investors. The program, which is open to all active investors, allows you to earn extra income if you refer a friend or another individual to the platform. You can find these referral links in the deposit/withdraw section of your account. Note that the amounts that you can earn from referrals vary and are briefly explained in the image below.

5% Skin in the Game

To mitigate risks, Grupeer has a feature that is technically known as 5% skin in the game. How does it work? Well, the credit companies (loan originators) must invest at least 5% in the loans they issue to ensure that the investors are safe. Again, the loan originators have to buy back from investors (through the buyback guarantee) if the borrower defaults or delays loan payments for a period exceeding 60 days.

Grupeer Investment Risks

Needless to say, some risks of investing in P2P platforms like Grupeer. In addition to defaults, there’s a possibility of Grupeer going bankrupt or a loan originator failing to buyback. While the buyback guarantee shields investors from defaults, things can become bleak if a loan originator goes bust and cannot afford to buy back. Although this has not happened on Grupeer yet, there’s a chance that it could happen.

So what can you do to mitigate the risks? No matter what you’re told, one of the best way to minimize your risks as an investor is to spread out your investments on as many loan originators, loans, and projects as possible. You can also go for loans with collaterals but this won’t be of much help if the loan originator goes bankrupt.

Is Grupeer safe?

There is no short answer to this. I can say that high risks equal high rewards and every investment carries risks with it. In Grupeer for instance, it’s only possible to send money to and from your bank account. This means that nobody can transfer money to their accounts even if they gain access to your bank account details. This is essential in keeping fraudsters at bay.

Also, always make sure to your do thorough due diligence.

Grupeer’s Ease of Use

Although the platform’s website looks a little bit flat and dated, it’s very easy to use and navigate thanks to its limited features. It’s also readable and mobile-friendly, but not very convenient if you’re looking for detailed information on projects and loans.

The platform is also available in various languages including English, Spanish, German, Russian, and French. Better still, the platform has commendable customer support. You can get in touch with them via email, phone or live chat.

Grupeer’s Main Competitors

Some of Grupeer’s competitors include Mintos, CrowdEstate, Estateguru, Crowdestor, Bulkestate and Flender.

Grupeer Pros

- Frequent cashback campaigns to boost your earnings;

- Large loan volumes and multiple loan originators;

- High interest rates (up to 14%, average 13,19%);

- Detailed investment information;

- The availability of auto-invest.

Cons

- No secondary market and early withdrawal;

- Small investment statistics;

- A relatively new platform;

- Indirect investment structure (You only invest through loan originators)

Conclusion

While there are a few drawbacks such as lack of secondary market, there is no shortage of viable investment options that pay high interests.

In essence, Grupeer is one of many P2P platforms out there. In addition to offering an average return of 13,19%, most loans are secured by buyback guarantee to ensure that your investments are secure at all times. The platform also gives you the chance to select your desirable projects. And if you do not have time to go through that hassle, the platform has the auto-invest feature to help you invest automatically.

But before investing your money in any of the projects, just take your time and do your research and only invest in projects that you’re comfortable with.

All in all, Grupeer seems to be a fast-growing crowdlending platform that is great for those looking for alternative investment options.